“Europe has lost more ground among the top 100 high-tech companies, but those that remain have strengthened their position,” highlights Axel Freyberg, partner at the international consulting firm AT Kearney and leader of the Communications, Media and Technology Practice in Europe, the Middle East and Africa.

In 2013, European companies generated 9% of the revenue of the top 100 companies across the nine high-tech segments. By 2015, this figure had fallen to 7-8%, following Microsoft's acquisition of Nokia's device business. During this period, European companies consolidated their positions in key areas.

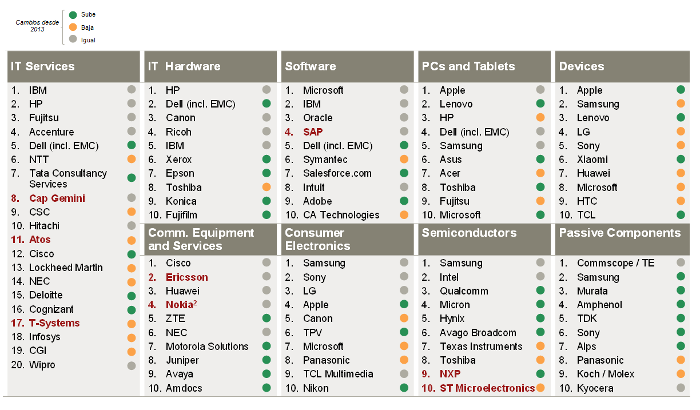

The nine high-tech segments included in the study are: technology services, technology equipment, programs and software, computers and tablets, devices, communication equipment and services, consumer electronics, semiconductors and passive components.

“Despite the many challenges on the continent, high-tech leaders have been able to focus, and have used mergers and acquisitions to strengthen their position in the large strong area of Europe: complex solutions in the B2B space,” says Javier Navarro, leader of the telecommunications practice at AT Kearney Iberia.

The merger of Alcatel-Lucent and Nokia, for example, has created a new European leader in the communications equipment and services sector. Europe continues to dominate the segment, with a 35-40 percent share of revenue among the top 10 companies. The semiconductor sector is another positive example of an area where Europe has improved, as NXP's acquisition of US-Freescale propelled the company into the top 10 in 2015.

AT Kearney's updated high-tech study (read here) shows that, on the one hand, European companies have strengthened their position through mergers and acquisitions, while on the other hand, the rise in the rankings of certain companies is hindering the recovery of European high-tech. For example, Lenovo now ranks third after acquiring Motorola, and Dell is fifth in services and software after its merger with EMC.

Given these challenges, how can Europe regain ground in the global high-tech sector?

“A new source of innovative products and competitive advantages is needed for Europe to recover. The Internet of Things represents a new opportunity that Europe could seize to further boost its high-tech sector, provided the right conditions are in place,” explains Javier Navarro.

As the latest study by AT Kearney shows, the Internet of Things (IoT) will create an €80 billion solutions market in Europe alone and will benefit systems integrators, service and platform aggregators, systems and software distributors, among many others.

Despite challenges in the components sector, Europe possesses many of the qualities needed to become a leader in the Internet of Things. Its strength in key vertical markets (such as healthcare, automotive, and industrial products), emerging IoT solution providers (e.g., ARM in chipset design), innovative creators (such as Riot OS, Arduino, and Raspberry Pi), and global leaders in communications equipment and services (such as Ericsson and Nokia) are just a few examples of what could propel European high technology to the forefront.

Javier Navarro is convinced: “With the right measures, the high-tech landscape in 2025 can be radically different, but we have to start now.”.

About the study:

A.T. Kearney has published two studies in recent years on the European high-tech sector. The first, “The Future of Europe’s High-Tech Industry” (2012), concluded that less than 10% of the revenue of the world’s top 100 high-tech companies (across nine segments) was generated by companies headquartered in Europe. The second, “Rebooting Europe’s High-Tech Industry” (2014), highlighted the minimal change in the revenue share of European-based companies, even though their number had fallen to nine according to 2012 financial reports. We have now updated the study with the latest available data and improved segmentation (which was released in December 2015).

1. Based on reported revenue from January 2015 to December 2015

2. Includes Alcatel-Lucent

Source: Capital IQ; AT Kearney