These technologies will never be able to offer multiple video-on-demand channels or 3D HD television [2], nor other advanced services that can be offered through fiber.

These technologies will never be able to offer multiple video-on-demand channels or 3D HD television [2], nor other advanced services that can be offered through fiber.

President Obama himself, as well as many other heads of state and executives of Western companies, have recognized that Next Generation Networks (NGNs) are one of the main keys to overcoming the current crisis, due to their capacity to generate employment in network construction and to build a more productive and sustainable economic fabric through their use. Governments have understood that broadband is a basic necessity, on par with electricity, gas, or water.

According to the FTTH Council's "FTTH Ranking" [4], 75 million FTTH subscribers were reached by the end of 2011, but only 10.3 million of them were in Europe. Although Europe has lagged behind North America and Asia, last year the number of homes connected to fiber grew by 41% and the number of subscribers by 28%. In terms of penetration, the ranking is led by Lithuania (28.3%), Norway (14.7%), and Sweden (13.6%). In terms of absolute number of users, Russia is the largest market with 4.5 million, followed by France, Ukraine, Italy, and Portugal.

The reality is that there is significant variation between countries in Europe, and unfortunately, Spain is not among the leaders, despite having operators with substantial investment capacity, such as Telefónica, Vodafone, and Orange. According to CMT data [5], Spain ended 2011 with a total of 171,177 FTTH lines, representing a 206.4% increase compared to 2010. Thus, of the 11,147,934 broadband lines in Spain, only 1.53% are fiber optic, most of which belong to Telefónica and GIT. What could be the solution to Spain's lagging FTTH deployment? In a typical FTTH deployment scenario, the majority of the operator's CAPEX is the cost of civil works, although the final investment depends on several factors (the possibility of deploying aerial fiber instead of underground, household density, availability of existing conduits, etc.). As we will see, open access optical networks offer the ability for multiple operators to simultaneously exploit the fiber commercially, minimizing the cost per home passed and accelerating the growth of the customer base. Therefore, it is the ideal solution for Spain to become a leader in this market, which will undoubtedly help the necessary change in the production model.

Business Models for Fiber Optic Networks:

European incumbent operators are quite reluctant to invest in FTTH (Fiber-To-The-Home), primarily due to existing regulations that require them to offer wholesale services to other operators at regulated, transparent, and non-discriminatory prices. Depending on the country, these sharing obligations range from conduits to services. European regulators believe that wholesale services facilitate competition. However, this can limit the ability to differentiate offerings and innovate, and has proven not to be an incentive to invest.

Taking advantage of this situation, smaller operators (such as Numericable in France or Optimus in Portugal) are trying to gain market share and differentiate their service offerings through fiber optic deployment. Similarly, small municipalities (like GIT in the Principality of Asturias), construction companies (like Emaar in Saudi Arabia), and electricity companies (like Dong Energy in Denmark or Eins Energy in Germany) are building open access networks and offering wholesale services to other operators with less capacity to reach the last mile.

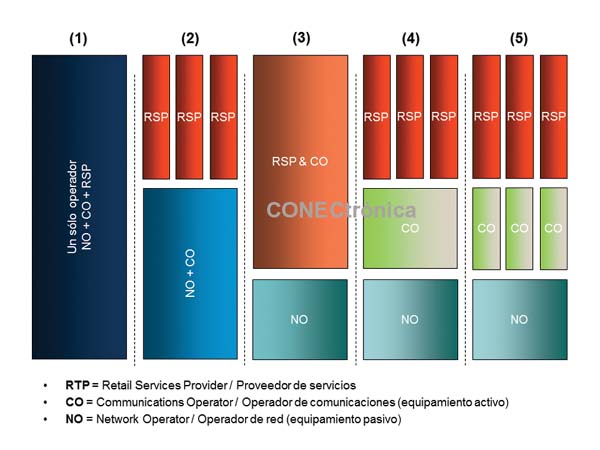

Thus, fiber optics has generated new business models, not only because of the services it can offer, but also because of the roles that the various agents investing in the construction and operation of the networks can assume. Typically, there are three types of roles, and an agent or operator can have one or more of them, as shown in Figure 1:

- The network operator (NO) is the operator that builds the passive physical infrastructure, that is, the cabling, fibers, splitters, cabinets, etc.

- The communications operator (CO) is the one that installs and operates the active equipment, providing connectivity to service providers.

- The service providers (RSPs) are those that control the end customers and market broadband services.

Open networks are those in which these three roles are assumed by different entities and have garnered significant interest in the industry, as they have been shown to accelerate the deployment of fiber optic networks, reduce the return on investment time, and foster competition. Without a doubt, open networks are the best deployment option in urban areas, until a significant user base is achieved; as well as in rural areas, as a long-term alternative.

Next, we will study in more detail the most successful FTTH network deployment models, focusing on those corresponding to open networks.

Model 1:

Incumbent operators in each European country (Telefónica in Spain, Orange in France, Deutsche Telekom in Germany, etc.) have historically followed Model 1 in older analog telephone networks and attempt to assume all three roles in their home markets for new fiber deployments. However, due to EU regulatory requirements, Model 2, 4, or 5 is actually being followed. That is, incumbent operators typically assume all three roles (NO, CO, and RSP) and, at the same time, offer both unbundling and bitstream services at regulated prices to other operators.

Telefónica is very interested in investing in FTTH in Spain to differentiate its services from its competitors, as its strategy has always been based on differentiation, thus offering more and better services to its customers. However, CMT regulations require Telefónica to replicate its fiber offerings below 30 Mbps—more than enough for most current services—and, furthermore, to continue maintaining its copper network for several years. Under these conditions, Telefónica is not willing to make an aggressive investment in fiber optics, especially since the consumption crisis is affecting households, which are opting for low-cost telecommunications plans. Telefónica would have to invest per household passed, while alternative operators that lease their network would invest per household connected, with much less investment and risk. The situation in Spain is, with some nuances, very similar to that in the rest of Europe

Verizon is probably the best example of an operator that single-handedly performs all the possible roles of a carrier and follows a Model 1 FTTH approach. Verizon's main driver for deploying fiber optics was to acquire a new customer base from cable companies, which were very successful in the United States. American regulations favored investment, as sharing infrastructure at regulated prices is not mandatory, unlike in Europe. This allows Verizon to exclusively sell the improved quality and services to end users, while also benefiting from lower operating and maintenance costs compared to copper.

Model 2.

Model 2, in which one operator manages the liabilities and assets (NO and CO) on which several operators offer services (RSP), has several advantages: more efficient use of infrastructure through sharing and a shift of competition from infrastructure to services. For this model to succeed, common open interfaces and clear SLA agreements are necessary.

European incumbent operators have been offering this wholesale or "bitstream" service over copper networks and will have to continue offering it over fiber networks. However, this model has proven ineffective in incentivizing investment, and if this trend continues, a possible solution would be to create a public network; after all, this is how the current copper networks were built. The neutral public operator provides the infrastructure and wholesale services (NO and CO) so that other operators can offer their own services (RSP) to citizens, who can then select the one that best suits their needs, following model 2. In this way, NGN services are introduced, and competition is encouraged in areas that are unattractive to private investment. As a Spanish example, we have GIT, a public operator belonging to the Principality of Asturias, whose mission is to launch, maintain, and operate the neutral FTTH network in rural areas of Asturias, known as Asturcón. In this case, unlike Singapore's Next Gen NBN, there can only be one RSP per household, although users can select the one that best suits their needs. The predominant RSPs in this network are Adamo and Telecable.

Another possibility, very similar to that of other utilities such as the electricity grid, would be for the public operator to invest in and manage only the passive infrastructure, including the buildings where the active equipment is located, and for the operators to act as both the CO and RSP, which would correspond to model 5. In this case, operators will compete not only on services but also on infrastructure. In fact, Sweden is following a similar model, with several municipalities promoting open networks. In Spain, this would mean providing work for much of the construction workforce, as well as acquiring some buildings so that operators could later install their active equipment. The maintenance and construction of these networks could be carried out by equipment manufacturers and service companies. The State would have a guaranteed return on investment in the very long term, both from rental income and from increased productivity and economic sustainability. A significant short-term investment would be necessary, but we are talking about a highly productive investment that would improve citizens' quality of life, unlike other construction projects that contribute no economic or social value.

Models 3 and 4:

Singapore made a strong commitment to accelerating the rapid development of FTTH networks with its Next Gen NBN (Next Generation Nationwide Broadband Network) plan. The goal was to build a subsidized, open access FTTH network to boost both competition and investment. The passive component was subsidized with $750 million, and the winning NO (Network Operator) was the incumbent operator SingTel and a group of companies forming Opennet. The subsidy for the active component (GPON equipment, IP routers, etc.) was $250 million, and the winning CO (Network Operator) was StarHub. Although SingTel seemed likely to win the CO RFP, its victory in the NO RFP and the requirement for the CO to be operationally separate from other service providers reduced its chances. The CO is subject to strict price controls and universal service obligations. Different providers, or RSPs, offer services simultaneously to each home over this active infrastructure. That is, in the same household: voice service can be contracted through RSP1, broadband internet access through RSP2, television and video on demand through RSP3, etc. In this case, a model 4 is being followed.

Furthermore, SingTel is also acting as a CO and RSP in the most commercially attractive geographic areas of Singapore, namely the most densely populated and affluent areas. In this case, we would be talking about a Model 3.

Model 5

corresponds to "unbundling" or disaggregation, where the dominant operator typically leases the passive infrastructure and central offices to the other operators. This model is widely used in Europe for copper infrastructure.

Model 5 could also be implemented through voluntary collaboration between operators, provided, of course, that it does not harm competition or lead to consumer abuse. This is what Vodafone and Orange are currently doing successfully in Spain in the mobile telephony sector. Vodafone and Orange divided their 3G network in Spain, collectively saving €300 million between 2007 and 2011. For the user, this collaboration is completely transparent, as the antennas are able to recognize customers of each company and connect them directly to their respective networks. According to data from the companies themselves, this sharing of sites translates into a 25% improvement in coverage in the affected areas and a 40% reduction in the number of installations. Undoubtedly, this model could also facilitate fiber optic deployments. For example, in France, Orange, Numericable, and SFR, despite competing with each other, signed an agreement in 2008 establishing the conditions under which the operators committed to sharing their deployed fiber optic network. This achieves much greater coverage at a much lower cost, without affecting competition, since users can choose between the three operators, and they can compete in both active infrastructure and services.

Technological Options for Open Optical Networks

Although solutions exist for unbundling (physical separation) over GPON, the simplest way to achieve this is through P2P Ethernet and WDM-PON. P2P Ethernet involves unbundling optical fibers, which is very similar to traditional copper networks where each subscriber receives a twisted pair of copper cables. WDM-PON, on the other hand, involves unbundling wavelengths, which can be easily implemented at the operator's headquarters, provided all active equipment from different operators is located in the same building. These three technologies also allow for bitstreaming (virtual separation) and even the use of different operators serving the same end customer, employing distinct Q-in-Q VLANs for each RSP and for each service within a single RSP.

P2P Ethernet [1] has been a very successful technology for creating open networks in Northern Europe (Sweden, Finland, the Netherlands, etc.), as it allows for very simple unbundling at the central office. In addition to the ease of performing local loop unbundling, several factors make P2P Ethernet very attractive, such as: higher bandwidths (100 Mbps or 1 Gbps dedicated to each user), the simplicity and familiarity of the Ethernet protocol, the ease of establishing QoS per service and user, and finally, security. However, Ethernet also has disadvantages compared to PON networks, the main one being cost, due to the need to deploy a fiber to each subscriber and use more active equipment (one port per fiber is required). This increased active equipment means more space in the central offices and higher energy consumption for the operator.

In contrast, GPON [6] is much more energy-efficient and requires less space and less fiber, perfectly adapting to the future requirements of operators, thanks to XG-PON (NG-PON1) and WDM-PON (NG-PON2). This is the main reason why the vast majority of FTTH deployments are being carried out with this technology. Furthermore, GPON allows for the creation of open networks via bitstream, although QoS management becomes more complex in this scenario [7]. Since in GPON the backbone fiber from the operator's central office to the splitter is shared by all users, the only way to perform unbundling is to install one backbone fiber per operator and one splitter per operator, requiring subscriber switching from one operator to another to be carried out outside the central office [7]. If there is only one splitter between the central office and the subscribers, the above process is relatively simple; however, most deployments in Spain typically employ two splitting stages [8].

WDM-PON [9] is the most attractive fiber optic access technology and is considerably simpler than other PON technologies. While it maintains the same point-to-multipoint architecture as TDM-PON at the physical layer, each user has a dedicated wavelength at the virtual layer, facilitating unbundling. In other words, it is equivalent to GPON at the physical layer and to P2P Ethernet at the virtual layer. Using WDM-PON in the access network offers other significant advantages over GPON and XG-PON: ease of providing guaranteed bandwidth without contention to each user and service, high bandwidth scalability, greater distances and splitting factors with fewer active and central equipment, simpler network management, operation, and maintenance, greater security, and lower latency.

Author:

Article provided by Ramón Millán

Bibliography

- [1] “Fiber Optic Broadband Technologies”. Training Manual No. 55, ACTA, 2010

http://www.ramonmillan.com/tutoriales/bandaanchafibraoptica.php

- [2] “3D HD IPTV: The ‘killer application’ for fiber optics?”. Ramón Jesús Millán Tejedor, BIT No. 179, COIT & AEIT, February-March 2010, p. 5.

http://www.ramonmillan.com/tutoriales/3dhdtv.php

- [3] “Fiber Optics is ‘in fashion’”. Ramón Jesús Millán Tejedor, BIT No. 187, COIT & AEIT, December 2011, p. 9.

http://www.ramonmillan.com/tutoriales/fibraopticabeneficios.php

- [4] “Reshuffling Europe's Fibre to the Home leadership. Leader Scandinavia may be overtaken by South and East Europe - West Europe lags”. FTTH Conference, Munich, 15 February 2012.

http://www.ftthcouncil.eu/documents/PressReleases/2012/PR2012_EU_Ranking_FINAL.pdf

- [5] “Monthly Note December 2011”. CMT (Telecommunications Market Commission), February 2012.

http://www.cmt.es/es/publicaciones/anexos/nota_mensual_diciembre_2011.pdf

- [6] “What is… GPON (Gigabit Passive Optical Network)”. Ramón Jesús Millán Tejedor, BIT No. 166, COIT & AEIT, December 2007, pp. 63-67.

http://www.coit.es/publicaciones/bit/bit166/63-67.pdf

- [7] “Open Access and Local Loop Unbundling on GPON Networks”. ECI Telecom, February 2009.

http://www.ecitele.com/OurOffering/Industries/Solutions/Solution%20Assets/open-access-and-local-loop-unbundling-on-gpon-networks.pdf

- [8] “Study on the feasibility of FTTH network deployment”. CMT, May 2009.

http://www.cmt.es/c/document_library/get_file?uuid=1f1abb96-6c08-4068-bf92-b697f164a03b&groupId=10138

- [9] “NG-PON (Next Generation Passive Optical Network)”. Ramón Jesús Millán Tejedor, Conectrónica nº 154, GM2 Technical Publications, February 2012.

http://www.ramonmillan.com/tutoriales/ngpon.php