One of the region's main characteristics is its heterogeneity: the involvement of national authorities varies considerably from country to country, as they may or may not include telecommunications infrastructure in their overall development strategy. On the regulatory side, there are no specific rules dedicated to improving superfast broadband in general, and FTTH/B in particular.

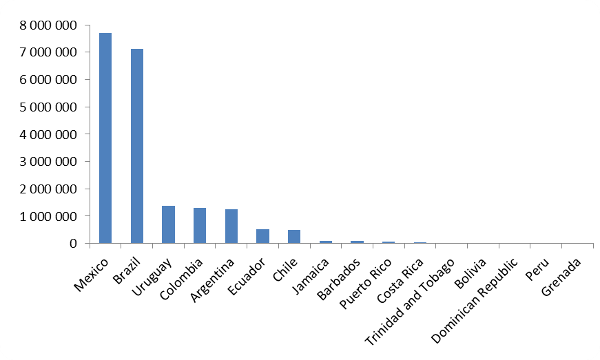

At the end of 2015, the largest FTTH/B market in Latin America was Mexico, which now slightly surpasses Brazil, with 1.29 million subscribers (compared to 1.25 million subscribers in Brazil). Together, these two countries account for more than 69% of the region's total subscribers. Another country that showed very interesting growth was Colombia, which now has more than 1.3 million households and 150,000 subscribers.

In the largest markets, competition appears to have had a positive impact and has actually encouraged FTTH players to expand and/or accelerate their deployments. This is the case, for example, in Brazil, Argentina, Mexico, and Chile. The types of players participating in FTTH can also vary significantly across countries. In some cases (Argentina, Mexico, Chile, Uruguay, etc.), traditional operators play a key role and are very active in this new market. But in most cases, the initial deployments have been initiated by smaller, private players, focused on limited areas, at least in the short to medium term. As an example, the Mexican market grew significantly during 2015, with a 46% increase in subscribers: competition between the two main players, Telmex and TotalPlay, appears to be driving the market positively. Meanwhile, the Brazilian market grew slightly less (32% increase) and is also being driven not only by strong participation from domestic players, but also by small players deploying in very localized areas.

Since 2013, we have seen the emergence of pan-regional players, particularly in the Caribbean islands. Cable & Wireless Communications, through its LIME brand, is a leading company in Barbados and Jamaica, where it is involved in FTTH deployments. Another player was a cable operator, Columbus Communications, which operates under the Flow brand in Barbados and Jamaica, as well as in Grenada and Trinidad and Tobago. In early 2015, Cable & Wireless acquired Columbus Communications and decided to offer its ultra-fast broadband services under the Flow brand in most markets. While DOCSIS 3.0 is the main infrastructure, the cable operator also launched some FTTH networks in smaller areas.

In larger countries, we can, of course, mention the Telefónica Group, which applies a strategy tailored to each market in which it operates. América Móvil is another major LATAM player through its Claro brand. América Móvil is also deploying both FTTLA + DOCSIS 3.0 and FTTH networks, depending on the country.

The participation of these pan-regional players could represent a significant opportunity for improving FTTH/B in the region. While not yet apparent, they could decide to adopt a common strategy in different markets, each supporting the other.

Generally speaking, the LATAM region has strong FTTH potential due to its demographics and the dynamism of its real estate market. However, it also faces challenges due to the fact that international interconnectivity is not always efficient. For example, in Bolivia, international interconnectivity is insufficient, which impacts the actual capabilities that ISPs are able to provide to their customers.

However, we have seen very positive signs for FTTH since 2013: the growth in both coverage (Homes Passed) and adoption rate (subscribers) is impressive (increases of 46% and 57% in 2014 respectively, followed by +27% and +39% in 2015). The FTTH offering seems to have found great success with end users. Most providers offer triple-play services that include television. And several providers launched 1 Gbps solutions a few months ago.

When comparing the LATAM region with other mature markets worldwide, it is clear that the potential is very high because the market is in a very early stage. But it is also worth mentioning that, in terms of penetration rates (number of subscribers over the total number of households in a country), 9 LATAM countries have entered the global ranking as of September 2015, with rates from 1.76% (Brazil) to more than 47% (Uruguay, where the penetration rate is even higher than in the leading European countries in the ranking).