Small modular reactors (SMRs), which are smaller, partially factory-built nuclear fission reactors, are frequently touted as the ideal solution for powering data center facilities. By delivering clean, continuous, and reliable power wherever it's needed, SMRs would seem to be the key to solving AI's energy needs, but how realistic is this new nuclear renaissance?

Analysts at IDTechEx have been closely monitoring trends in both data center infrastructure and emerging energy technologies, and the new report, "Small Modular Nuclear Reactor (SMR) Market 2026-2046: Technologies, Players, Benchmarking, Forecasts," highlights the developments of the most promising SMR projects, with a data-driven benchmarking framework for 10 different reactor types and 20-year forecasts for the SMR market, broken down by technology and region.

SMRs have the potential to become an integral part of the global electricity production mix for data centers and the overall power grid, and are projected to reach more than 1900 TWh of annual electricity production by 2046.

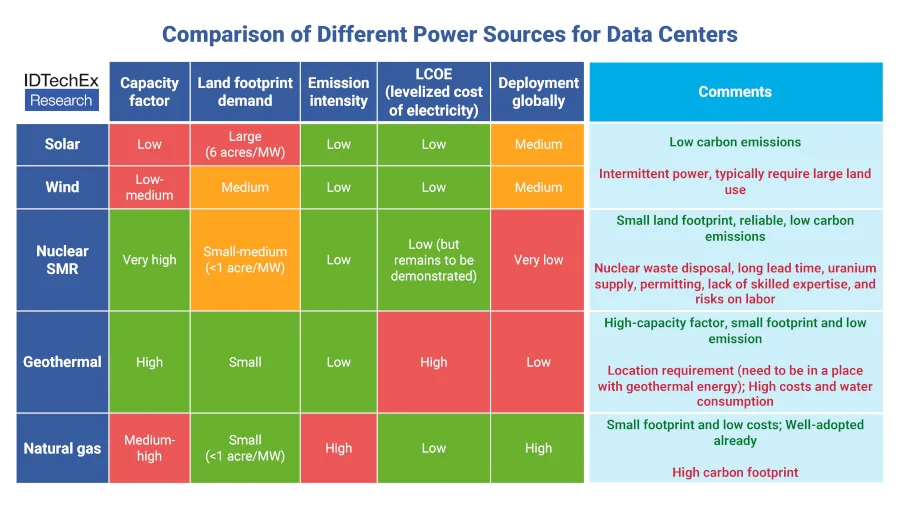

Comparison of different power sources for data centers. Image source: IDTechEx

Why SMR for data centers?

The core value proposition of small nuclear power plants (SMRs) revolves around the fact that by reducing the size of nuclear power projects, they are far less likely to experience the significant cost overruns and construction delays that are common in the traditional nuclear industry. Their lower power output (typically under 300 MWe) and smaller footprint also mean they can be installed in a more flexible range of locations, delivering electricity much closer to the data center where it is needed and becoming operational much faster than larger energy infrastructures.

In the SMR market, economies of scale are shifting from relying on the size of each plant (as in a large conventional nuclear project) to being based on the manufacture of larger volumes of individual SMRs. Mass production of SMRs has the potential to offer highly competitive levelized cost of energy (LCOE), especially considering that nuclear power is continuously available, unlike intermittent renewable energy sources—a critical requirement for data centers.

The reality, however, is that the first prototype of an SMR design (FOAK) will likely be expensive. Most SMR developers agree that overcoming this inertia and committing to the production of at least 6 to 10 units of the same reactor design would reduce costs by up to 40% compared to the FOAK. Evidence of this can be found in similar learning curves demonstrated in the manufacture of small nuclear reactors for submarines.

The role of data center hyperscalers

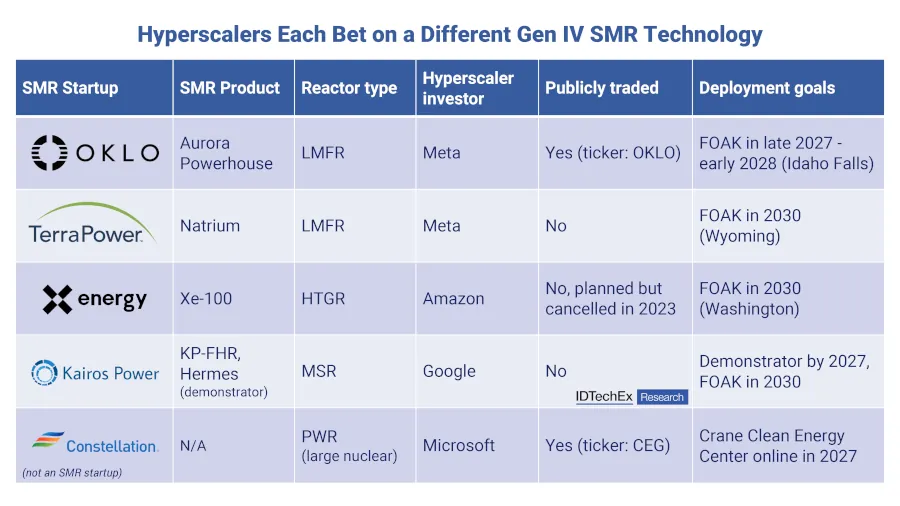

Data center hyperscalers like Microsoft, Amazon, Google, and Meta are among the few private organizations with sufficient financial resources to fund not just individual data centers, but entire fleet projects. By 2026, these agreements are already taking shape, with each hyperscaler making commitments to various nuclear power developers.

SMR designs can be categorized according to their different reactor technologies, with three of the most promising concepts being high-temperature gas-cooled reactors (HTGRs), liquid metal fast reactors (LMFRs), and molten salt reactors (MSRs). It is therefore likely no coincidence that Google, Amazon, and Meta have made significant commitments to SMR startups, each developing a different type of reactor technology: Google with the MSR startup Kairos Power, Amazon with the HTGR developer X-Energy, and Meta with two different LMFR startups: Oklo and TerraPower.

HTGRs, LMFRs, and MSRs are referred to as fourth-generation (Gen IV) nuclear reactor designs.

In its comprehensive SMR market report, IDTechEx compares these reactor types using a quantitative benchmarking framework. The assessment is based on parameters such as industry interest, safety and efficiency to compare these Gen IV types with each other and also with more established Gen III+ nuclear reactor technologies, such as pressurized water reactors (PWRs) and boiling water reactors (BWRs).

SMRs will not be a "quick fix," but a long-term strategy

Before getting too excited about the prospect of nuclear-powered data centers, it's important to consider the timelines involved. Even the most prolific SMR startups, such as Kairos Power, X-Energy, and TerraPower, anticipate that it will take until around 2030 for their first fully operational SMR to begin supplying electricity. Even if delays are avoided, it's important to note that these targets refer to the first-of-a-kind (FOAK) deployment. A larger-scale rollout to reach gigawatts of power will take at least a few more years.

By comparison, the data center industry anticipates that a significant electricity shortage could hinder development as early as 2028. Simply put, SMRs won't be the solution to the looming power shortage in data centers in the short term. However, this doesn't mean they can't become a critical piece of long-term infrastructure.

Although gas-fired power plants will be the primary source for meeting energy needs in the coming years, recent global events have highlighted the volatility of oil and gas markets. Nuclear SMRs offer a flexible and scalable solution for supplying low-carbon energy to data centers, using fuel that can be easily stored.

Data center hyperscalers have become organizations with capital rivaling that of small nations. The IDTechEx report on small modular nuclear reactors (SMRs) analyzes how governments and data center giants are investing in these reactors to future-proof their electricity demand, in a market that could reach $53.8 billion by 2036 and nearly $300 billion by 2046.